Scorecards’ and Rating Models’ regular validation is vital for the optimal function of the decision tools. The operating environment of the models is not stable. Changes may come from various factors such as systems, policies and processes, customers’ profiles, behaviour patterns, economic environment, competition, marketing initiatives, etc. Thus, regular Scorecards’ validation is imperative in order to identify any shifts in the models’ performance and decide on potential actions.

One of the side-effects of the 2008 Financial Crisis was the increasing interest by Supervisory bodies on the models’ Development and Validations practices followed by Banks, for which directives, guidelines and consulting papers are routinely being issued since. The use of models for Provisioning purposes, as part of the adoption of the IFRS 9 Standard, further increased the importance of a regular and holistic Validation process for those models.

Furthermore, independency on the Validation Function has now become a prerequisite, along with the the establishment of multiple and independent Validation levels: Validation by the (internal) Validation Unit, by the internal Audit Unit, by third parties.

Why StatDec?

StatDec Scorecards’ and Rating Models’ Validation Services are customized to the model type and use of the Model. They include statistical tests and performance metrics commonly used in the industry, while more advanced statistical approaches are employed where needed. Furthermore, the Validation Framework may be customized to the Client’s specific requirements, such as existing validation framework, specific tests and support in coding for internal monitoring.

StatDec Validation Services are not just an array of statistical tests. Though usually emphasis is placed on the statistical side, we introduce in the validation process a business perspective by aiming to answer on questions such as:

- Is the model being used properly?

- Is the model discriminating risk?

- Are the decisions optimal?

- Are the risk estimates by score accurate?

- Are the estimates on client’s profile accurate?

- What are the next steps?

The aim is to provide knowledge and insights on the functions of the Validated Models but also on what is happening on the Portfolios themselves.

The validation tests are conducted as separate blocks.

| Qualitative | Quantitative |

|---|---|

| Score Inputs & Data Processing | Discrimination Power |

| Data Quality & possible limitations | Accuracy |

| Model implementation accuracy | Distribution Stability |

| Exclusion Analysis | Concentration Analysis |

| Definitions review | Model Inputs Analysis |

| Model Use | Model Use |

When examined as a whole, one can understand what is happening in the Portfolio.

Findings on systems, policies, marketing activities and collections can be identified and presented as part of the Scorecard Validation. In many occasions, focused analysis will take place based on findings throughout the analysis so as to track the mechanisms and reasons behind the observed patterns.

Results are intuitively benchmarked to expectations, as set on the specific portfolio but also making use of market experience on similar portfolios.

Validations are accompanied with a proposed customized action plan based on the findings of the analysis. Best practices are recommended, that are not necessarily restricted to Models’ changes.

The use of StatDec Validation Services allows for an expert and in-depth validation of an organization’s Model inventory. In situations that an independent validation or an additional validation layer is required, StatDec can support Businesses with professionalism and deliverables of the highest quality.

Unlock the power of data with propensity models, for more informed decision-making!

Propensity models can forecast customer behavior, enabling you to make data-driven marketing, sales, and product development.

Propensity models are statistical models that predict the likelihood of a customer taking a certain action, such as making a purchase, responding positively to a campaign or churning. These models can be used to improve business performance in a number of ways, including:

- Acquiring new customers: By identifying customers who are more likely to convert, businesses can focus their marketing efforts on the right people.

- Retaining existing customers: By understanding what factors lead customers to churn and turn to competitors, businesses can take steps to reduce churn rates (attrition or churn models)

- Cross-selling and upselling: Propensity models can be used to identify customers who are likely to be interested in additional products or services (conversion models)

- Customer segmentation: Propensity models can be used to segment customers into groups based on their likelihood of taking certain actions. This information can be used to create targeted marketing campaigns.

- Personalizing the customer experience: By using propensity models to segment customers, businesses can create more tailored and relevant offers and promotions.

- Risk assessment: Propensity models can be also used as inputs to risk scores (e.g. credit risk, etc.).

- Cost Efficiency: Maximize your marketing budget by targeting only those prospects with a high likelihood of responding positively. This leads to cost savings and a more efficient allocation of resources.

- Competitive Advantage: Stay ahead of the competition by leveraging data-driven insights that your rivals may not be utilizing to the same extent.

Our approach is a unique blend of advanced analytics, machine learning, and deep expertise in implementable solutions, tailored to your specific needs, as it includes:

- Methodology design based on review of requirements, processes, data definition, data availability and implementation environment.

- Data review, management and preparation

- Creation of quality definition and development sample

- Examine all the potential variables that will be considered under the development process (systemic variables and derived/transformed ones, dynamic vs. static, etc.)

- Model development (use of Machine Learning algorithms or more conventional approaches)

- Model validation in independent sample – as part of the development (if possible)

- Full Documentation on model development, including probability tables (strategy tables)

- Support in model implementation

With StatDec’s propensity models, you will improve your customer targeting, and be able to optimize your marketing and sales strategies.

Scoring models and analytics are widely used by telecommunication (Telco), Internet and Energy providers for an efficient management of their client base and support expansion to new client segments.

Models are built to answer specific questions of the organization, such as what is the probability of a client to leave (churn models), will a client pay the bill, propensity of customer reaction to an event, etc.

Furthermore, MIS design allows to track business KPI, adjust to market events and make better use of the data already available in the organization.

Models for Energy and Telco providers usually cover the following topics:

- Risk & Default

- Attrition or Churn Probabilities

- Response , Cross-Sell, Renewal

- Profitability and Lifetime Value

- Utilization of Limit

- Fraud

- Propensity (customer reaction to an action)

Why StatDec?

With 30 years of experience in developing and supporting predictive models, StatDec is a reliable and experienced partner that can support Telco and Energy providers to make knowledge out of their data and implement data-driven decision models and strategies.

Usual benefits from StatDec's analytic services in Telco and Energy providers may fall in the following categories:

- Ability to Automate & Standardize Actions

- Targeted Customer Approach

- Cost Reduction

- Pro-active Strategies

- Allowance for Champion : Challenger business culture

- Measurable Results

- Closer portfolio monitoring and data management

- Collections efficiency

Services / Scoring

Model Validation Services

Independent, rigorous, and business-aware validation of credit scoring, rating, and risk models — aligned with the ECB and EBA regulatory framework.

Regular validation of Scorecards and Rating Models is vital for the optimal functioning of decision tools. The operating environment of models is not stable — changes arise from systems, policies, processes, customer profile shifts, behavioural patterns, the economic environment, competition, and marketing initiatives.

The 2008 Financial Crisis triggered increasing supervisory scrutiny of model development and validation practices. The subsequent adoption of IFRS 9 and the full roll-out of CRR3 have further reinforced the importance of a holistic, independent, and multi-layered validation framework. Independence of the Validation Function is now a regulatory prerequisite, encompassing internal Validation Units, Internal Audit, and independent external validators.

Regulatory Framework for Model Validation

StatDec’s validation methodology is fully aligned with the current ECB and EBA regulatory framework. Institutions subject to SSM oversight must ensure validations cover both quantitative performance and qualitative governance dimensions, across all three lines of defence.

The most comprehensive revision of the ECB’s supervisory guide since TRIM, incorporating CRR3 (effective 1 January 2025). Key validation implications for Significant Institutions:

- Refined internal validation and audit expectations, explicitly integrated with the EBA IRB Validation Handbook

- New section on ML models — explainability, bias testing, and higher-frequency audit for complex models

- Senior management and management body directly accountable for model quality and ECB submission readiness

- LGD Reference Value elevated to an active validation challenge requiring documented action when weaknesses appear

- IRB permissions now granted at exposure class level (CRR3) — institutions must document clear model strategies

- 3-month implementation deadline for material model changes post-ECB permission; outsourcing does not exempt from validation

- ECB announces increase in proactive internal model investigations in areas of high supervisory attention

- Market risk split into separate CRR2 and CRR3 chapters reflecting phased FRTB implementation

- EBA/GL/2023/01Guidelines on Internal Model Risk Management — overarching governance, documentation, and periodic review obligations for all internal models.

- EBA IRB Validation HandbookEBA’s supervisory handbook on IRB rating system validation, now explicitly incorporated into the ECB’s revised July 2025 Guide.

- EBA/GL/2017/16Guidelines on IRB PD, LGD and EAD estimation — Full Validation requirements, backtesting standards, and Margin of Conservatism.

- EBA/GL/2022/14Guidelines on IRRBB and CSRBB — model validation obligations for EVE and NII models, behavioural assumptions and stress scenarios.

- EBA/GL/2020/02Loan Origination and Monitoring — validation of creditworthiness assessment models, including AI/ML tools used in origination.

- CRR3 / Reg. (EU) 2024/1623In force January 2025 — selective IRB approach, revised roll-out and PPU rules, updated parameter floors and CCF treatment.

Validation Types

Full Validation vs. Ongoing Monitoring

Regulatory frameworks and sound model risk management practices distinguish between two complementary validation regimes. StatDec supports both with appropriate depth and rigour.

Full Validation

A comprehensive, end-to-end review covering conceptual soundness, data integrity, development methodology, implementation accuracy, and ongoing performance. Required by the ECB Guide (July 2025) and EBA/GL/2023/01 at defined intervals or upon material model changes.

Triggered by:

- Initial model deployment and regulatory approval

- Material changes to model design, data inputs, or scope

- Deterioration in ongoing monitoring metrics

- Regulatory environment changes (e.g. CRR3 alignment requirements)

- Periodically per model risk policy — typically every 3 years for IRB

Periodic / Ongoing Validation

Annual or semi-annual performance reviews focused on stability, discrimination, and calibration accuracy. Designed to provide early warning of model drift and inform remediation decisions before a Full Validation cycle is triggered.

Components include:

- Discrimination and rank-ordering (Gini, KS, AUC)

- Population Stability Index (PSI) and characteristic drift

- Calibration accuracy and backtesting

- Exclusion and override analysis

- Action plan tracking from prior validations

Post-Implementation Review

Conducted 6–12 months after deployment of a new or materially changed model. Verifies live performance and implementation accuracy, aligned with the ECB’s 3-month implementation deadline introduced in July 2025.

- Implementation accuracy assessment

- First-cycle performance benchmarking

- Data pipeline and integration review

- Early indicator monitoring setup

Targeted / Thematic Validation

Focused deep-dive on a specific dimension of model risk, commissioned in response to supervisory findings, audit observations, or specific business concerns.

- Data quality and representativeness

- Definition of default alignment (CRR3/EBA)

- Margin of Conservatism (MoC) review

- LGD Reference Value challenge

- Override and exception policies

Test Framework

Validation Test Blocks

Validation tests are structured as independent blocks. When examined holistically, they provide a complete picture of both model health and underlying portfolio dynamics. Findings on systems, policies, marketing activities, and collections can be identified and presented as part of the validation output.

Expanded Model Coverage

Beyond Credit Risk: Non-Credit Model Validation

The regulatory validation mandate extends well beyond credit scoring. EBA guidelines and Pillar 2 requirements impose validation obligations on provisioning models, treasury risk models, liquidity models, and behavioural models integral to the institution’s risk management framework.

IFRS 9 ECL models carry direct P&L impact and are under increasing scrutiny from auditors and supervisors. StatDec provides independent validation covering all model components and the macro-economic overlay framework.

SICR Models

Validation of Significant Increase in Credit Risk criteria for Stage 1→2 migration, including relative/absolute PD change approaches and qualitative backstop triggers.

Lifetime ECL Component Models

Full validation of point-in-time PD term structures, downturn LGD estimates, and EAD/CCF models — including conversion from TTC to IFRS 9 PiT parameters.

Forward-Looking Information & Overlay Models

Assessment of macro-economic scenario design, probability weighting, and satellite models linking macro variables to PD and LGD.

Portfolio-Level & Collective ECL Models

Validation of grouping criteria, loss emergence period assumptions, and benchmarking of collective provisions against actual loss experience.

Governed by EBA/GL/2022/14 on IRRBB and CSRBB, institutions must validate models for interest rate risk in the banking book, including behavioural models critical for accurate EVE and NII sensitivity computation.

Non-Maturity Deposit (NMD) Models

Validation of core deposit volume stability, repricing assumptions, and behavioural maturity estimates, benchmarked against EBA supervisory outlier thresholds.

Loan Prepayment Models

Assessment of prepayment speed assumptions for fixed-rate retail and corporate loans, with sensitivity analysis across interest rate scenarios and credit quality strata.

EVE & NII Sensitivity Models

Review of interest rate shock and stress scenarios (per EBA standard shocks), repricing gap methodology, and alignment with supervisory benchmarks.

CSRBB Models

Validation of credit spread risk in the banking book, including spread sensitivity measurement and scenario design for securities portfolios.

Liquidity risk models underpin LCR, NSFR, and ILAAP requirements. Their validation ensures that stress outflow assumptions and behavioural parameters remain conservative and realistic.

Regulatory Liquidity Ratio Models

Validation of inflow/outflow rate assumptions, HQLA haircut methodology, and classification of liabilities and committed facilities under stress conditions.

Liquidity Stress Testing Models

Assessment of scenario design (idiosyncratic, market-wide, combined), survival horizon computation, and behavioural assumptions on deposits, credit lines, and collateral calls.

Deposit Run-Off Models

Validation of segmented run-off rates for retail, SME, and institutional deposits, reviewed against historical crisis observations and regulatory floors.

Internal Liquidity Adequacy Models

Independent review of ILAAP liquidity buffer sizing, risk appetite metrics, and models supporting internal liquidity transfer pricing.

StatDec’s validation expertise extends to the broader model inventory relevant to risk management and capital planning, including the ML-specific validation expectations introduced in the ECB’s July 2025 Guide.

Internal Models for Market Risk (IMA)

Validation of VaR, Expected Shortfall, and stress VaR models, including backtesting under FRTB/CRR3. Separate CRR2 and CRR3 treatment per ECB July 2025.

Machine Learning Models

Specialist validation of ML-based credit risk and fraud models addressing explainability (SHAP, LIME), bias testing, and governance — aligned with ECB July 2025 and EBA/GL/2020/02.

ICAAP / Stress Testing Models

Review of internal capital adequacy models, Pillar 2 add-on estimation, macroeconomic stress scenario design, and capital projection models.

Propensity & Behavioural Models

Validation of early warning systems, pre-approval propensity, customer lifetime value, and churn prediction models used in commercial decision-making.

Why StatDec

Our Validation Approach

Regulatory Alignment

All validations are designed in full alignment with the ECB Guide (July 2025), EBA guidelines, and CRR3 requirements, ensuring defensible, supervisory-ready findings.

Business Perspective

Beyond statistical metrics, we assess whether models are being used properly, decisions are optimal, and risk estimates are fit for business purpose.

Customised Frameworks

Validation scope, tests, and reporting are tailored to the client’s existing framework, portfolio characteristics, and specific regulatory context.

Portfolio Insights

Validation outputs include portfolio-level findings — shifts in borrower behaviour, policy effects, and market changes — not just model-level statistics.

Independent External Validator

As a specialist external validator, StatDec satisfies the independence requirement under EBA/GL/2023/01 for institutions requiring a third validation layer.

Actionable Outcomes

Every validation concludes with a structured, prioritised action plan — with best practice recommendations extending beyond model changes to governance and process.

Commission an Independent Validation

Whether you require a Full Validation under the ECB’s July 2025 Guide, ongoing monitoring, or validation of IFRS 9, IRRBB, or Liquidity models, StatDec delivers expert, independent assessments of the highest quality.

Get in Touch

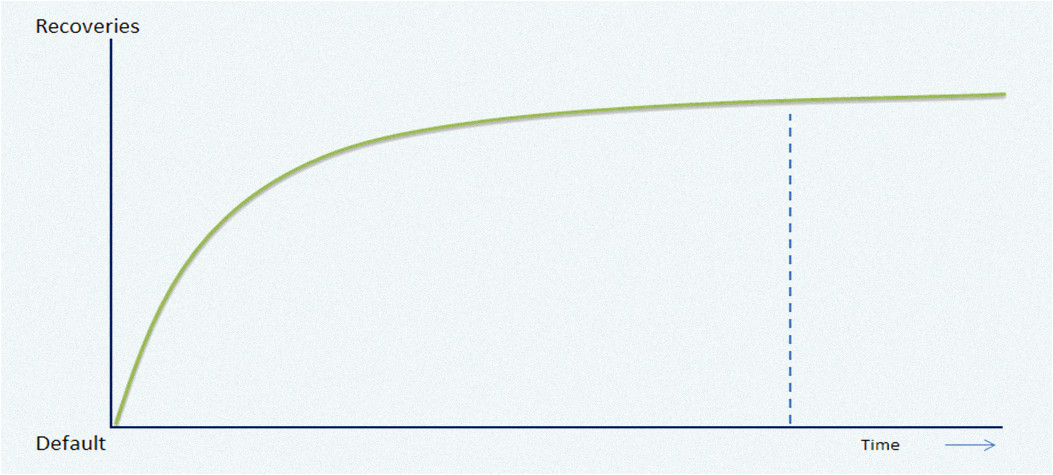

The need for valuation of a retail portfolio usually occurs when a portfolio is to change ownership.

Typical such engagements take place in cases of merges & acquisitions and when a portfolio or a segment of it is in selling process (debt sell).

Participants in this process require a fair and accurate estimation of future cashflows of the portfolio so as to estimate it's present value and set a price.

Statistical Decisions approach in estimation is based on long experience in analyzing behavioir patterns in retail portfolios and consists of the following elements:

- Data quality and process review for deciding on whether data represent full and concise information for the analysis

- Identification of key drivers for future cashflows or recoveries

- Benhmakring vs reference expectations

- Model or segmentation approach for portfolio cashflows estimation for lifetime of fixed time horizon